How Do I Read My Insurance Policy?

There are a lot of complexities in reading an insurance policy. It can feel overwhelming and it can feel daunting. Why? Legal language and complex terms make it hard to fully take in and read an insurance policy. However, here are a couple tips to read your policy and to help you understand your insurance policy:

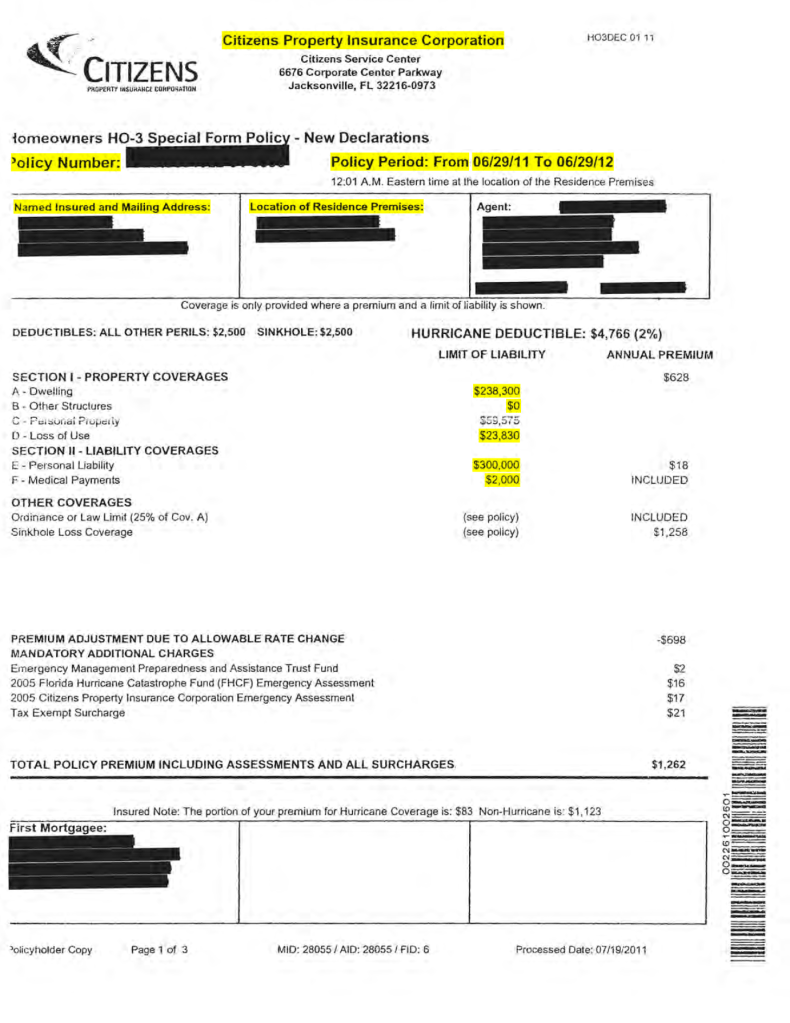

Cover Page: This page typically includes basic information such as your policy number, the effective date, and the expiration date. It also specifies the types of coverage you have purchased. Understand the timeline and dates of your policy properly.

Coverage Sections: Your policy will outline the specific types of coverage you have, such as liability, property damage, medical payments, etc. Each section will detail what is covered, any exclusions, limits of coverage, and conditions that apply. Perils that are covered in an insurance policy vary on HO-3, HO-5, HO-6, Renters Policy, and so forth. The standard policy is HO-3.

Exclusions: This section lists situations or circumstances where your policy will not provide coverage. It’s crucial to understand these exclusions to avoid surprises when filing a claim. A few exclusions that are commonly denied in a claim are wear/tear, seepage, rot, neglect, and long term damage. These are a few exclusions to consider. .

Limits and Deductibles: Your policy will specify the maximum amount the insurance company will pay for covered losses (policy limits) and the amount you must pay out of pocket before your insurance coverage kicks in (deductibles). Here is an example, if your policy had a limit of $50,000 for the Dwelling portion of your policy and the repairs are $100,000. The insurance carrier will only pay you the policy limit which is $50,000. The deductible kicks in and is applied so based on our example instead of $50,000 with a $1,000 deductible, the carrier will pay you $49,000. This makes sense. Now, be mindful of your policy notes, for example if your deductible is percentage based then it would apply differently.

Here is a different example, if your policy limit is $500,000 for Coverage A on your Dwelling and your deductible is 5% that means your deductible is $25,000. If you have a claim and it falls under the amount then you will not get compensated. Typically you will see a percentage based deductible on earthquake, flood, hurricane, and certain specialty policies. It doesn’t mean you shouldn’t check your standard policy because it can exist. I and many other adjusters have seen this. It is best to review your policy prior to filing a claim to understand your limits and deductibles.

Endorsements or Riders: These are additions or amendments to your policy that modify the coverage provided. Endorsements can expand coverage, add exclusions, or change policy terms. Be sure to review any endorsements carefully. This is key for jewelry and specialty personal property that an insured owns.

Cancellation and Renewal: This section outlines the circumstances under which the insurer or the policyholder can cancel the policy and the process for renewal.

Contact Information: Your insurance policy should include contact information for the insurance company, including phone numbers, mailing addresses, and website URLs for claims reporting and customer service.

Readability: Some insurance policies are written in dense legal language, while others are more consumer-friendly. If you’re having trouble understanding your policy, don’t hesitate to contact your insurance agent or the insurance company directly for clarification.

Ask Questions: If you’re unsure about any aspect of your policy, don’t hesitate to ask questions. Your insurance agent or representative should be able to provide explanations and guidance.

Before you file a claim, contact your local Public Adjuster and we can assess your policy. We will read it in detail and provide feedback. Claim Commander Inc. provides free consultations and assessments for your insurance claim.

Remember, it’s essential to review your insurance policy regularly, especially when major life changes occur, to ensure it still meets your needs and provides adequate coverage.