The Palisades Fire, which erupted in January 2025, had devastating and disastrous effects on Los Angeles, resulting in the destruction of over 16,000 structures and the loss of at least 29 lives. The fire severely impacted communities such as Pacific Palisades, Malibu, and Topanga, leading to significant challenges in recovery and rebuilding.

Community Impact and Recovery Efforts

In the aftermath, residents faced difficult decisions regarding rebuilding or relocating. Factors influencing these choices included emotional attachments, financial considerations, and the increasing risk of wildfires in the region. The recovery process has been complex, with homeowners navigating uncertainties and costs associated with reconstruction.

What costs? Some are analyzing the best method for debris removal and allocating funds to begin the repair process efficiently. Homeowners have to be mindful of the different phases occurring for the repair process. Each phase has to address the environmental hazards and debris while also being mindful of the upcoming debris removal on the property.

Some carriers are maintaining the proper procedure and protocol while others do not have a standard to address this. Each homeowner should take the time to research their rights and the insurance company requirements before proceeding forward.

Heritage and Conservation Challenges

The fire also destroyed historic structures, notably at Will Rogers State Historic Park and Topanga State Park. Conservationists are now focusing on preserving the cultural fabric of the city while integrating fire-resistant and climate-resilient practices into restoration efforts.

Legal and Infrastructure Issues

Legal actions have emerged, with residents filing lawsuits alleging that downed municipal power lines may have caused the fire. The Los Angeles Department of Water and Power initially claimed the lines near the fire’s origin had been disconnected for years but later admitted they were energized at the time of the fire.

Business Closures

The disaster also led to the permanent closure of iconic establishments, such as Duke’s Malibu, an oceanfront restaurant that succumbed to the combined effects of the fire and subsequent flooding.

If you have a business, you have a different avenue of coverages that need to be addressed. Examples would be business interruption, damaged inventory, rent expenses, employee lost wages, and extended business interruption.

It is imperative for anyone going through an insurance claim to seek professional advice from experts. Contact us at 877-605-8429. We are your local Public Adjusters and care deeply about bringing the neighborhood back to a healthy and safe community.

Getting back on your feet after a major life event—whether it’s a natural disaster, financial setback, or other personal challenges—can feel overwhelming. For families, the process involves not just recovery but also re-establishing a sense of stability and support for everyone involved. The steps you take now can help restore peace of mind and strengthen bonds as you work together to rebuild.

Here’s a simple guide for families on how to take proactive steps to recover and start fresh. While every situation is unique, these principles can help create a foundation for moving forward with hope and resilience.

1. Ensure Safety First

Evacuate if you haven’t already: Make sure all individuals are safe and away from the site.

Avoid entering the property until it’s deemed safe by authorities (fire department or other experts). Hazardous conditions may persist, such as structural damage, smoke inhalation, or potential electrical issues.

Color tagged – A lot of properties have different color tags reflecting the safety of occupancy in the property.

2. Temporary Housing and Living Expenses

If your home is uninhabitable, ask your insurer about temporary living arrangements. Many policies cover living expenses like hotel stays, meals, and transportation.

Keep receipts for all extra living expenses and share them with your insurance company.

3. Contact An Advocate: Public Insurance Adjuster or Attorney

Notify your insurer immediately to report the fire and initiate your claim. They will guide you on what documentation and steps are needed.

Handling insurance claims are multifaceted. It can feel overwhelming and place a level of concern.

Keep in mind, an advocate should have your best interest at heart.

Ask about temporary housing options if your home is uninhabitable and inquire about emergency assistance funds.

4. Secure the Property

Board up windows and doors to prevent further damage or theft.

If you can safely do so, cover exposed areas (e.g., using tarps for the roof or windows) to prevent rain or weather from causing more harm.

5.Review Your Insurance Policy

Familiarize yourself with your policy’s coverage for fire-related damages. Make sure you understand your deductible, limits, and exclusions. If you have an advocate, they will guide you through the process.

If you have any questions or don’t agree with the initial claim assessment, you can request an independent review from your insurance company with your advocate.

6. Document the Damage

Take photos and videos of the damage before cleaning or removing anything. Document all areas affected (even those with smoke damage).

Make a list of all damaged or destroyed property, including personal items, furniture, appliances, and electronics. This will be essential for your claim.

Don’t throw anything away unless it’s a safety or health hazard, as it may be needed for inspection by your insurance adjuster.

If you have previous photos, videos, and paperwork that show the state of the home, this will be a good benefit.

Remember, the more detailed the inventory list, the more beneficial.

7. Contact a Fire Restoration Company

Hire a professional fire damage restoration service to assess the property. They will start the cleanup and restoration process, which can help prevent further damage from soot, smoke, or water used in firefighting efforts.

8. Meet with the Insurance Adjuster

Your insurer will assign an adjuster to inspect the damage. Be prepared to provide them with your documentation (photos, lists, receipts).

If possible, have a contractor or restoration expert with you to ensure that all damage is properly assessed.

9. Salvage and Replace Belongings

Start making decisions about what can be salvaged, repaired, or replaced. For electronics and other appliances, you may need to work with specialists to determine if they are safe to use.

Work with your insurer to confirm any replacement or repair coverage for your personal property.

10. Start the Restoration Process

During the insurance claim or if it is settled, start working with contractors to rebuild or repair your home. This may involve structural repairs, painting, replacing flooring, or handling mold and smoke damage.

Stay in touch with your adjuster for updates and ensure you follow up on any changes or additional damages that might arise during the rebuilding phase.

11. Smoke Claim Procedures

Smoke claims will require specific testing. Stay involved with your advocate and insurance company to get proper testing throughout the house.

Stay in touch with your adjuster for updates and ensure you follow up on any changes or additional damages that might arise during the smoke cleaning phase for your structure and personal property.

Claim Commander Inc. Public Adjusters Elkhorn, Nebraska

Claim Commander Inc. Public Adjusters is your Public Adjuster in the following Elkhorn, Nebraska zip codes 68007, 68022, and 68069. We maximize property claim settlements while saving you money, in addition we offer great service, return phone calls, and are only a phone call away.

At Claim Commander Inc. our goal is to ensure the insurance company pays you – the policyholder – enough money to rebuild any and all property damage sustained to your home or business while providing the highest level of professional service.

Our claims staff will work to protect homeowners and business owners manage their claims, and fully document their losses in order to maximize their financial interest in all insurance claim settlement returns.

Our goal is to reduce the emotional and financial burden placed upon you as the result of damage to your personal and real property.

Insurance Claim Settlement Services – Public Adjuster Elkhorn, Nebraska

Claim Commander Inc. is dedicated to addressing all of your property damage insurance claim needs as your public adjuster. Each property loss or insurance claim is unique and Claim Commander Inc., your Public AdjusterElkhorn, Nebraska will work diligently to determine the extent of your loss.

New Insurance Claim

Have you had an insurance loss in the last year and have not yet filed an insurance claim?

Give us a call today for your free consultation. We’ll discuss the claim with you, and whether it makes sense to use our services. We may also decide it’s best to come to the property and do an inspection of the loss, which is also free.

The earlier you contact Claim Commander Inc. regarding a free consultation of your insurance policy and likelihood of coverage by your insurance company, the better you can ensure you meet all your obligations under your insurance policy. Among other things, a homeowner or business policyholder has the duty to mitigate property damage and prepare a scope of loss & estimate of damages.

What are some of the mistakes homeowners make when reporting claims themselves:

They don’t understand the cause of the loss, so it gets misreported and denied.

They fail to recognize the total scope of the loss, and get underpaid.

They don’t document the loss properly and get underpaid.

They rely on contractors who are unskilled in insurance documentation, leading to underpayment or denial.

They fail to understand their obligations under the insurance policy, leading to denial.

Our highly trained, licensed public adjusters will guide you through the process of preparing and filing an insurance claim in a professional manner. Similar to how you would hire an attorney if you needed to go to court, or hire a certified public accountant to file your tax return, you should only file an insurance claim with your own professional insurance and construction expert – a Claim Commander Inc. Public Adjuster.

Pending Insurance Claim

Claim Commander Inc. Public Adjusters can intervene on your behalf at any point during the claims process and see to it that your claim gets resolved promptly. We work directly with your insurance company and its representatives to make sure they give your claim the attention it deserves. Our team of public adjusters – insurance and construction experts – advocate on behalf of your interest under the insurance policy and will not quit until you get the benefits to which you are entitled.

If you have received an offer for your insurance claim, we can take over from here. We re−document and cross-reference every aspect of your property damage or loss and usually find many things that were not originally included and other things that were not properly valued. Insurance Claim Adjusters are often very busy, have a vested interest in lowering property claim payments (i.e., to increase their own company’s bottom line), and sometimes overlook certain areas that can inadvertently reduce an insurance claim. We consistently deliver superior results for our clients, significantly better than original insurance company offers and, by deliberately handling fewer claims with higher settlement numbers, more care and attention to your particular claim than competitors.

Here is a list of the following items that are usually withheld on each insurance claim settlement:

Operation and Profit: Insurance companies withhold an extra 20% of your claim. Many policyholders do not realize that carriers must include this expense in the total property claim if a general contractor is involved in the repair process.

Content manipulation: Insurance companies intentionally withhold moving time to remove all items out of a room in order to complete necessary repairs.

Paint: Insurance companies sometimes overlook the application of 2 coats of paint, or the application of primer.

Base Service Charges: Insurance companies sometimes overlook additional funds for job site prep, travel time, delivery of goods, set up, take down of equipment.

Emergency Service Invoices: Insurance companies sometimes overlook any emergency costs accrued during the time of the loss (e.g., tarping a roof, buying a shop vacuum, renting dehumidifier, time to clean up loss, hotel stay, renting a storage unit).

With the application of these items, among others, Claim Commander Inc. Public Adjusters can get thousands, or tens of thousands, more than your initial offer. Our services are free until you are paid for your insurance claim.

If you have suffered a catastrophic property loss in Elkhorn, Nebraska we know how difficult these times can be for you and your loved ones. We have a team of support specialists who will assist you during this fragile time. You can rest assured knowing that with Claim Commander Inc. Public Adjusters on your side, you’ll get the results you are entitled to under your insurance policy.

Our highly trained, licensed public adjusters will guide you through the process of preparing and filing an insurance claim in a professional manner. Similar to how you would hire an attorney if you needed to go to court, or hire a certified public accountant to file your tax return, you should only file an insurance claim with your own professional insurance and construction expert – a Claim Commander Inc. Public Adjuster.

Re-Open Insurance Claim

Even though your claim has been settled, you may still be entitled to additional benefits. Insurance companies often times fail to properly determine the extent of losses in an insurance claim rendering a claim evaluation that is lower in value than what policyholders ought to be paid. Claim Commander Inc. Public Adjusters will take a look at your loss settlement for free and determine if you are owed more than your settlement offer.

We have successfully handled hundreds of insurance claims that carriers had already closed, and in many cases, we found benefits not assessed in the original evaluation. It would be in your best interests to see if we can do the same for you.

Nebraska has very good laws that usually allow you to re−open an insurance claim if you were not fully compensated. We offer a FREE CONSULTATION. We are paid only if we find areas of underpayment and/or items that were left out of your insurance claim settlement.

Most states allow you to re-open a claim at anytime up to 1 year after the loss occurred.

Even if you have received a check you can re-open the claim for additional funds.

We will review your claim for free if you feel that you did not receive a fair settlement.

Your initial offer may only be based on what is seen during a preliminary inspection of the premises. Many times there are hidden damages that are discovered during repairs. It is crucial to document the additional damages so you may receive the proper settlement.

You even have coverage for additional living expenses occurred during construction such as the following:

Permit costs

Architectural fees

Code Upgrades: this is crucial as your local code inspector could mandate major upgrades by law.

Electrical Usage: you could have coverage for a higher electric bill due to construction costs.

Finally, coverage for a final house cleaning once repairs have been complete

Get started on your FREE ONLINE POLICY REVIEW or call us toll free if you would prefer @ 1-877-605-8429 EXT 101.

What is the best way to prepare ourselves for a tornado?

This is never a fun conversation, but it is an important conversation that we must always think about during periods of high storm damage, tornado damage, or inclement weather that will affect your home, livelihood, and family. Here are an initial list of steps to conduct,

Stay Informed: Keep track of weather forecasts and warnings. Tornadoes can develop quickly, so having access to up-to-date information is crucial. Weather apps, NOAA Weather Radio, and local news stations are good sources.

Have a Plan: Create a tornado emergency plan for your household or workplace. Know where to seek shelter and have multiple options in case one becomes inaccessible. Practice your plan regularly, especially if you have children.

Identify Shelter: The safest place during a tornado is a basement or storm cellar. If that’s not available, seek shelter in an interior room on the lowest floor of a sturdy building, away from windows. Bathrooms, closets, or under stairwells are often good options.

Build a Tornado Kit: Put together an emergency kit with essential supplies like water, non-perishable food, a first aid kit, flashlight, batteries, blankets, and a portable weather radio. Make sure everyone in your household knows where it’s located.

Secure Your Property: Regularly maintain your home and yard to minimize potential tornado damage. Trim trees and bushes, secure outdoor furniture and objects that could become projectiles, reinforce garage doors, and consider installing impact-resistant windows or shutters.

Create a Communication Plan: Ensure everyone in your household knows how to communicate during and after a tornado. Designate an out-of-state contact person for family members to check in with if separated.

Stay Alert: Keep an eye on the sky and be attentive to weather alerts. Tornadoes can form rapidly, so don’t wait for an official warning if conditions seem threatening.

During a Tornado Warning: If a tornado warning is issued for your area, take immediate action. Seek shelter in the lowest level of your building, preferably in a small, windowless room at the center, away from exterior walls.

Protect Yourself: Cover your head and neck with your arms or a sturdy object to protect against flying debris. Use mattresses, blankets, or pillows for additional protection if available. Wait until authorities announce that the tornado warning has expired and it’s safe to leave your shelter. Be cautious when exiting, as there may be hazards such as downed power lines or debris.

These are just a list of a few items. Lets deep dive into the first few items on the list.

Stay Informed During Tornado Season

Listen to you local news stations, stay in touch with neighbors, and follow meteorologist information. There are a few YouTube channels that do a great job of tracking these storms. They have been helpful during periods of time that we experience intense weather conditions and patterns.

If you are in doubt, move yourself to a safer location immediately.

What does this mean? Where does your family meet in a scenario like this? Do you have a secondary location outside of your house if everyone is scattered around town. What if cell phone towers are knocked down? What would you do?

Set up an interior plan for the family. Meet in the basement or a safe location designated in your home. Provide a secondary meet up location and if you can a tertiary option. Providing multiple plan routes are important and effective for the safety of the entire family.

Who will be in charge if the main point of contact isn’t there or available? Provide scenarios and do a drill as a family on a nice weekend. Preparation is always key in these scenarios.

Build A Tornado Kit During Storm Season

What is comprised in a tornado kit?

Flashlight, batteries, food, water, tent lights, whistles, LED Flashlights, more batteries, poncho, headlamps, and even more items. Reach out to us if you have any questions about dealing with storm damage.

Our office line is 877-605-8429, ext 101 to reach our premier public adjuster.

Email us at claimcommander@gmail.com and info@claimcommanderinc.com.

What To Do If Insurance Doesn’t Give Enough Funds For Your Tornado Claim?

Here are a few tips for our community in Elkhorn, Nebraska; Bennington Lakes, Nebraska; Minden, Iowa; and any other community affected by the recent tornadoes.

Document. Document. Document. Lets get into this message. What does that mean? It means attention to detail. For repairs, walk around your exterior home and notice what is damaged and what is not damaged. For example, how many roofs have blown off or maybe the entire roof flew off or maybe a tree fell into your house? Regardless, all of this has to be presented properly to your insurance adjuster. Look at roof shingles, siding, gutters, windows, doors, framing, and any other exterior aspect. Now lets move into the interior part of the home, how do you assess and evaluate this properly? Think of an entire room from a wide perspective and analyze from top to bottom. A great Public Insurance Adjuster should be able to provide a detailed scope of repairs for the interior and exterior of the home.

If you have a business loss there are a few other items to consider. It goes beyond the structure especially if you do not own the structure, then you have to analyze the other portions of your business. Contact us to get a free assessment to get all of the details for your business loss insurance claim.

Prevent further damage. What does that mean? Do everything in your capability to provide further damage in your property. Your insurance company doesn’t expect you to re-shingle your own roof, but if there’s a gaping hole, they do expect you’ll take “reasonable steps” to prevent further damage. Draping a tarp overhead might be a viable solution. Obviously if your entire property is gone then begin the process for a proper debris cleanup.

Personal property have to be documented thoroughly. Line by line by line. How? There are inventory sheets that need to be filled out in great detail. Contact us to give you an assessment to conduct your personal property inventory and get your claim properly evaluated. You want to account for your items so you are indemnified properly. Your contract is meant to indemnify you after an insurance loss.

Get solutions, answers, and reaponses in writing. This is key when working with a Public Insurance Adjuster, there are responses and protocol that needs to be in writing. This is essential. WRITING and PROPER DOCUMENTATION will help you in the long run for an insurance claim. Over documenting or asking for phone conversations in writing will benefit you through this process.

Time for an insurance claim. This can vary, by this I mean if one home only has a few shingles to replace compared to another home that needs to reframed from the ground to the roof. These are two drastically different time frames for repairing the home. These two different claims would affect the time frame to settle the claim. The latter claim may need supplements or just multiple inspections to verify the repair process is tracking along properly. If you feel the claim is attempted to be settled and you do not have enough funds to finish the repair for the claim. Call us immediately, we will conduct a free inspection and furthermore we will address the fair repair value to get your back to pre-loss condition.

We are here to help and support the communities in distress. We are here to be your advocate. We listen and provide support through this period of damage.

What to do if my insurance won’t cover all of my tornado damage?

We must take a moment to understand that during periods of distress and natural disasters there are multiple efforts to assist homeowners, insured’s, business owners, and any personnel that file an insurance claim. Here is a list of things to do immediately,

Check for injuries: Check yourself and others for injuries. Administer first aid if necessary, but remember to only attempt to provide assistance if it’s safe to do so.

Watch out for hazards: Be cautious of any hazards such as broken glass, downed power lines, or damaged buildings. Avoid entering damaged buildings until authorities have deemed them safe.

Listen to authorities: Follow the instructions of local authorities and emergency services personnel. They will provide guidance on evacuation routes, shelters, and other important information.

Assess the damage: Once it’s safe to do so, assess the damage to your property. Take photos or videos of any damage for insurance purposes.

Contact loved ones: Let your loved ones know that you’re safe. If you’ve been separated from family members, try to establish contact with them as soon as possible.

Seek shelter if necessary: If your home has been severely damaged or is unsafe to stay in, seek shelter at a designated evacuation center or with friends or family.

Turn off utilities: If you suspect any damage to your home’s gas, water, or electrical lines, turn off the appropriate utilities.

Listen for updates: Stay tuned to local news and radio stations for updates on the situation and any additional safety information.

Help your neighbors: Check on your neighbors, especially those who may need assistance such as elderly or disabled individuals.

Document damage: Document any damage to your property by taking photos or videos. This will be important for insurance claims.

Now here are options to consider if you do not receive enough funds from your insurance company.

Contact your local Public Insurance Adjuster. We have an office in Omaha, Nebraska that services all of Nebraska and Iowa. Claim Commander Inc. assists personnel through these types of damages. We document the repair process, we itemize your personal property list, and we work with your insurance carrier to find you a proper place to stay. The additional living expense portion of your policy provides the support for housing, food, and unexpected expenses during a time of difficulty.

There are local groups that can provide funds or food for periods of time. Typically local news channels, radio stations, and shelters.

FEMA is another option. FEMA provides certain requirements before they can move forward with your application. Here are some details below,

To help FEMA assess your application, you can provide several insurance-status documents based on your claim and correspondence from your insurance company, including:

Denial of your claim letter: Proof that you are not covered under your insurance company and policy.

Settlement letter: What damage and property are covered by your insurance policy.

Delay letter: Proof of no official decision by your insurance company on your claim, and it has been more than 30 days from the time that you filed your insurance claim.

FEMA determines what help you may be eligible for based on the specifics of each FEMA application, including the documentation provided.

FEMA has a local number in your area that can be of further assistance.

How Do I Repair My Home Properly AfterA Tornado?

Shop around for contractors. Keep in mind there are typically only a limited amount of contractors that work with all of the current damage in the area. Get quotes and make sure you are hiring someone that is capable of the job. These jobs require a large scope of repairs: reframing, replacing roofs, replacing siding, interior water damage, flooring, replacing windows & doors, and the list goes on and on. Hiring a Public Insurance Adjuster takes away these concerns. We can do the research with you. Claim Commander Inc. typically will do the research with you to find the best team to repair your property.

Keep in touch as we provide further details about the other necessary steps to properly go through an insurance claim after tornado damage.

How do I address water intruding into my property?

Identify the source of the problem. A leak entering your home is frustrating, exhausting, and at times can be a stressful ordeal. Keep in mind the water does not always come from directly above. Water is intrusive and once it is trapped underneath your shingles, it brings a major effect to the sheathing/ roof decking. If this area is compromised, it is imperative to address it immediately especially if it is compromised.

1. Identify the Source: Try to locate where the leak is coming from. This might not always be directly above where you see water dripping inside, as water can travel along beams or rafters before dripping down.

Remember, safety is paramount when dealing with a leaking roof. If you’re unsure about accessing your roof or performing any repairs, it’s best to leave it to the professionals. Hire a roofer if you’re not comfortable assessing. Some investigations require an engineer to look into the damage further. The structure of the home may be built in a manner they will give you further insight into the damages.

2. Contain the Leak: Place buckets or containers under the leak to catch the dripping water and prevent further damage to your home’s interior. Also, prevent the home exterior, by tarping the roof. Some homeowners will do a temporary or immediate repair to prevent any further damage.

3. Mitigate Interior Damage: If there’s water pooling on the floor, use towels or a wet/dry vacuum to remove it. Move any furniture or belongings away from the leak to prevent further damage.

Hire a mitigation company to address the interior damages, typically drywall and flooring are affected. These need to be remediated immediately. If not, this will leave stains and excessive damage to your property.

4. Inspect Attic (If Accessible): If you have access to your attic, carefully inspect the area to see if you can identify the source of the leak. Look for wet spots, water stains, or signs of mold or mildew growth. Wet insulation in the attic needs to be addressed, usually by removing and replacing the damaged insulation.

5. Temporary Patch: If the leak is minor and you’re able to access the roof safely, you may be able to apply a temporary patch to stop the leak until a professional can assess and repair it properly. This could involve using roofing tar, roofing cement, or a patching kit designed for temporary repairs.

If you are not comfortable with patching the roof. Hire a professional roofer to handle repairs. Which brings us to the next point.

6. Contact a Professional Roofer: Roof leaks often require professional repair to ensure they are fixed correctly and to prevent further damage. Contact a licensed roofing contractor to inspect the roof, identify the cause of the leak, and provide a permanent solution.

7. Document Damage: Take photos of the leak and any resulting damage.

8. Filing a Claim: If you choose to file an insurance claim because of the damages, make sure to contact your local public adjuster before proceeding forward. Roof claims are complex and there are many steps to address a fair claim.

There are a lot of complexities in reading an insurance policy. It can feel overwhelming and it can feel daunting. Why? Legal language and complex terms make it hard to fully take in and read an insurance policy. However, here are a couple tips to read your policy and to help you understand your insurance policy:

Cover Page: This page typically includes basic information such as your policy number, the effective date, and the expiration date. It also specifies the types of coverage you have purchased. Understand the timeline and dates of your policy properly.

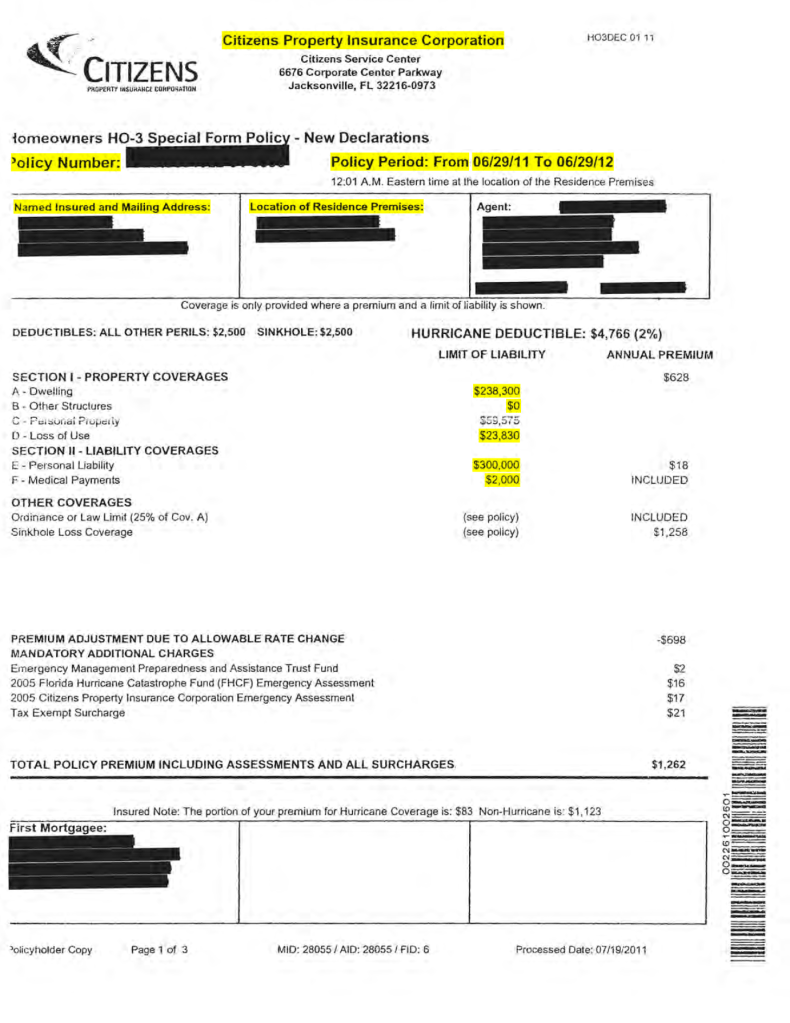

Coverage Sections: Your policy will outline the specific types of coverage you have, such as liability, property damage, medical payments, etc. Each section will detail what is covered, any exclusions, limits of coverage, and conditions that apply. Perils that are covered in an insurance policy vary on HO-3, HO-5, HO-6, Renters Policy, and so forth. The standard policy is HO-3.

Exclusions: This section lists situations or circumstances where your policy will not provide coverage. It’s crucial to understand these exclusions to avoid surprises when filing a claim. A few exclusions that are commonly denied in a claim are wear/tear, seepage, rot, neglect, and long term damage. These are a few exclusions to consider. .

Limits and Deductibles: Your policy will specify the maximum amount the insurance company will pay for covered losses (policy limits) and the amount you must pay out of pocket before your insurance coverage kicks in (deductibles). Here is an example, if your policy had a limit of $50,000 for the Dwelling portion of your policy and the repairs are $100,000. The insurance carrier will only pay you the policy limit which is $50,000. The deductible kicks in and is applied so based on our example instead of $50,000 with a $1,000 deductible, the carrier will pay you $49,000. This makes sense. Now, be mindful of your policy notes, for example if your deductible is percentage based then it would apply differently. Here is a different example, if your policy limit is $500,000 for Coverage A on your Dwelling and your deductible is 5% that means your deductible is $25,000. If you have a claim and it falls under the amount then you will not get compensated. Typically you will see a percentage based deductible on earthquake, flood, hurricane, and certain specialty policies. It doesn’t mean you shouldn’t check your standard policy because it can exist. I and many other adjusters have seen this. It is best to review your policy prior to filing a claim to understand your limits and deductibles.

Endorsements or Riders: These are additions or amendments to your policy that modify the coverage provided. Endorsements can expand coverage, add exclusions, or change policy terms. Be sure to review any endorsements carefully. This is key for jewelry and specialty personal property that an insured owns.

Cancellation and Renewal: This section outlines the circumstances under which the insurer or the policyholder can cancel the policy and the process for renewal.

Contact Information: Your insurance policy should include contact information for the insurance company, including phone numbers, mailing addresses, and website URLs for claims reporting and customer service.

Readability: Some insurance policies are written in dense legal language, while others are more consumer-friendly. If you’re having trouble understanding your policy, don’t hesitate to contact your insurance agent or the insurance company directly for clarification.

Ask Questions: If you’re unsure about any aspect of your policy, don’t hesitate to ask questions. Your insurance agent or representative should be able to provide explanations and guidance.

Before you file a claim, contact your local Public Adjuster and we can assess your policy. We will read it in detail and provide feedback. Claim Commander Inc. provides free consultations and assessments for your insurance claim.

Remember, it’s essential to review your insurance policy regularly, especially when major life changes occur, to ensure it still meets your needs and provides adequate coverage.

Understand the Policy: Review the insurance policy to understand what is covered and what isn’t. Knowing the policy details will help set realistic expectations. Document the Incident. Fill Out Forms: Assist in filling out any claim forms required by the insurance company. Double-check that all information provided is accurate and complete.

Understand Settlement Offers: If the insurance company offers a settlement, help the person understand the terms and whether it adequately covers their losses. They may need to negotiate for a better offer if necessary.

Appeal if Necessary: If the claim is denied or if the settlement offered is insufficient, assist in preparing an appeal. This may involve providing additional evidence or arguing the case more persuasively.

If you have a family member, friend, or an associate. How can you be there for them? Listen to them and provide aid, support, and guidance.

Insurance claims aren’t always the easiest to settle, but with the right support, guidance and advocates you can get back to pre-loss condition.

If there are injuries, seek medical assistance immediately.

Only enter the property if it’s deemed safe to do so by authorities.

Contact Authorities:

Call emergency services to report the fire.

Notify the fire department for inspection and investigation.

Notify Relevant Parties:

Inform family members, friends, and neighbors about the situation.

Contact a Public Insurance Adjuster to report the fire and begin the claims process. A licensed and certified adjuster can be your advocate through the claims process.

Document Damage:

Take photos or videos of the damage for insurance purposes.

Make a detailed list of damaged or destroyed items.

Pro Tip: Prior to a fire, go around your home semi-annually and document your entire home. Load the video onto the cloud or another hard drive specifically a safe location. If you have important documents do the same.

Secure Property:

Board up windows and doors to prevent unauthorized entry. Contact a restoration company to assist to complete this task properly.

Cover damaged areas to protect against further exposure to elements.

Arrange Temporary Accommodation:

Find temporary housing for you and your family if the property is uninhabitable.

Check if your insurance policy covers temporary housing expenses. Signing with a Public Adjuster, they can assist you to properly read your insurance policy.

Utilities and Services:

Contact utility companies to suspend services or arrange for reconnection.

Notify post office, banks, and other relevant institutions of your temporary address.